This paper has dissected these core components, elucidating how each contributes uniquely to the overall value of an option. Through detailed analysis and graphical representations, we've demonstrated the distinct behaviors of IV and TV across various strike prices and their implications for trading strategies.

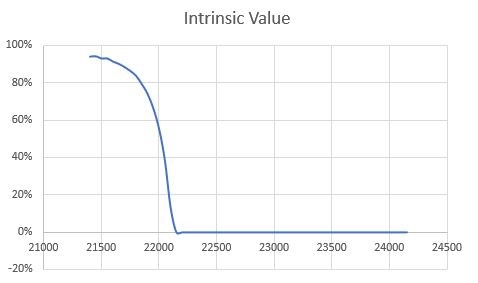

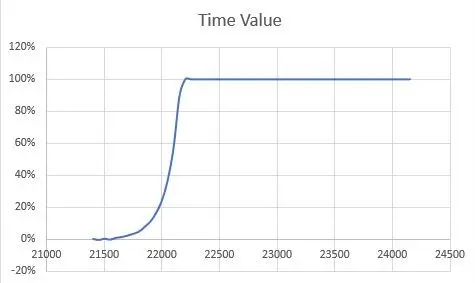

IV provides the essential value of an option when it is in-the-money, underscoring the actual profit that could be realized if the option were exercised immediately. Understanding this component helps traders assess the direct worth of their options based on current market conditions. On the other hand, TV encapsulates the potential future profitability of an option, factoring in the time remaining until expiration and the underlying asset's volatility. This speculative aspect of the premium is crucial for strategies that rely not just on the immediate price movements, but on the anticipated fluctuations over time.

The interplay between IV and TV is critical in shaping options trading strategies. Decisions regarding strike selection, timing of entry and exit, and the hedging of positions are all influenced by an understanding of these values. Moreover, the decay of TV as options approach expiration highlights the importance of timing in options trading, making it imperative for traders to not only choose the right positions but also to time their trades effectively.

Future research, as outlined, will further refine our understanding of these components by integrating factors such as implied volatility, interest rate changes, and cross-asset behaviors, which could lead to even more nuanced trading strategies. Additionally, advancing quantitative models and dynamic hedging techniques will aid traders in managing complex portfolios more effectively, adapting to market changes in real-time.

In conclusion, the dynamic nature of IV and TV offers both challenges and opportunities in options trading. By continuing to delve deeper into these aspects, traders can develop more sophisticated strategies that enhance profitability and manage risk more effectively. The ongoing study of these elements will undoubtedly continue to play a pivotal role in the evolution of financial markets.